FactSet: When High Quality Becomes Deep Value

FactSet is down 58% in 12 months. My economic model sees ~84% upside.

Over the past few months, I’ve been quantitatively analyzing dozens of high-quality companies using my economic financial model to identify clear dislocations between price and value.

One of them — and so far the cheapest within my universe — is FactSet Research Systems. ( FDS 0.00%↑ )

The company operates under a SaaS model, with recurring revenue and a 91% retention rate. It acts as a “digital library” and an essential navigation system for the global financial community, offering an open platform that integrates a vast sea of market data with the analytical tools needed to manage investments.

In short: it’s like Bloomberg.

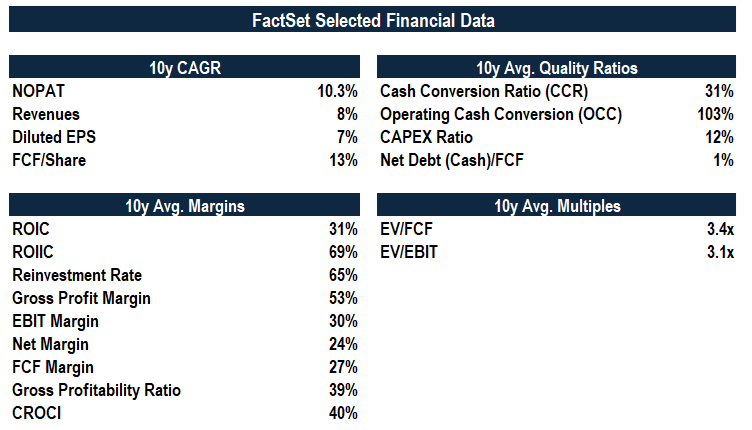

FactSet is a very good business — a toll bridge, as Buffett would say. Let’s just look at the numbers over the past 10 years (these are averages, not normalized figures):

These results clearly show that FDS is a high-quality company. In my model, the business has traded at average multiples of ~3x over the past decade (for example, ~3.4x EV/FCF and ~3.1x EV/EBIT on a 10y average).

If you look at traditional accounting metrics, the picture usually looks very different — double-digit multiples, according to Fiscal.ai data.

Here’s the key: my multiples are calculated on an economic, not accounting, basis — using normalized operating profits and adjusted FCF. That’s how I prefer to evaluate businesses.

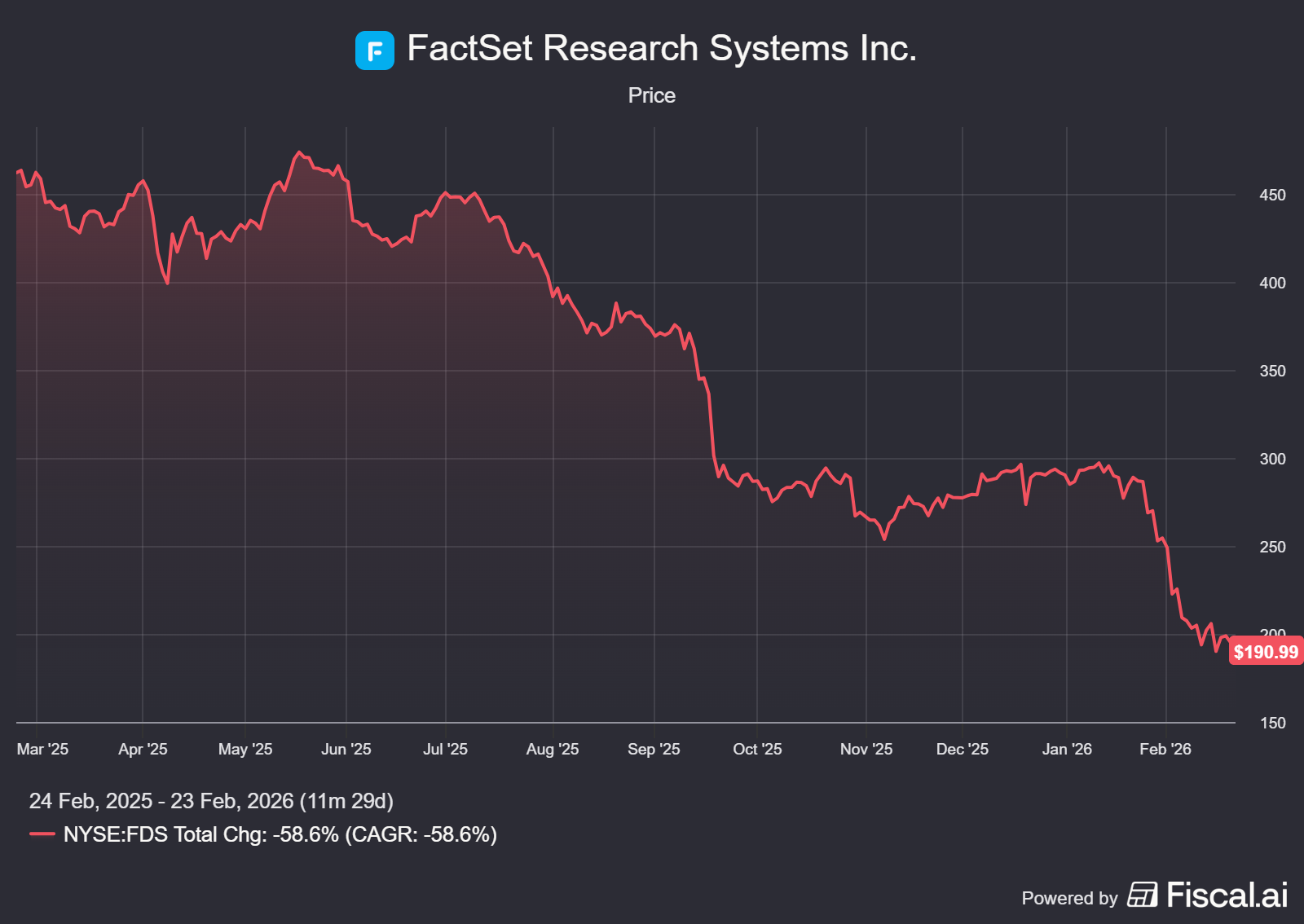

I like to assess companies over the long term — but over the past 12 months, FDS has declined 58.6%.

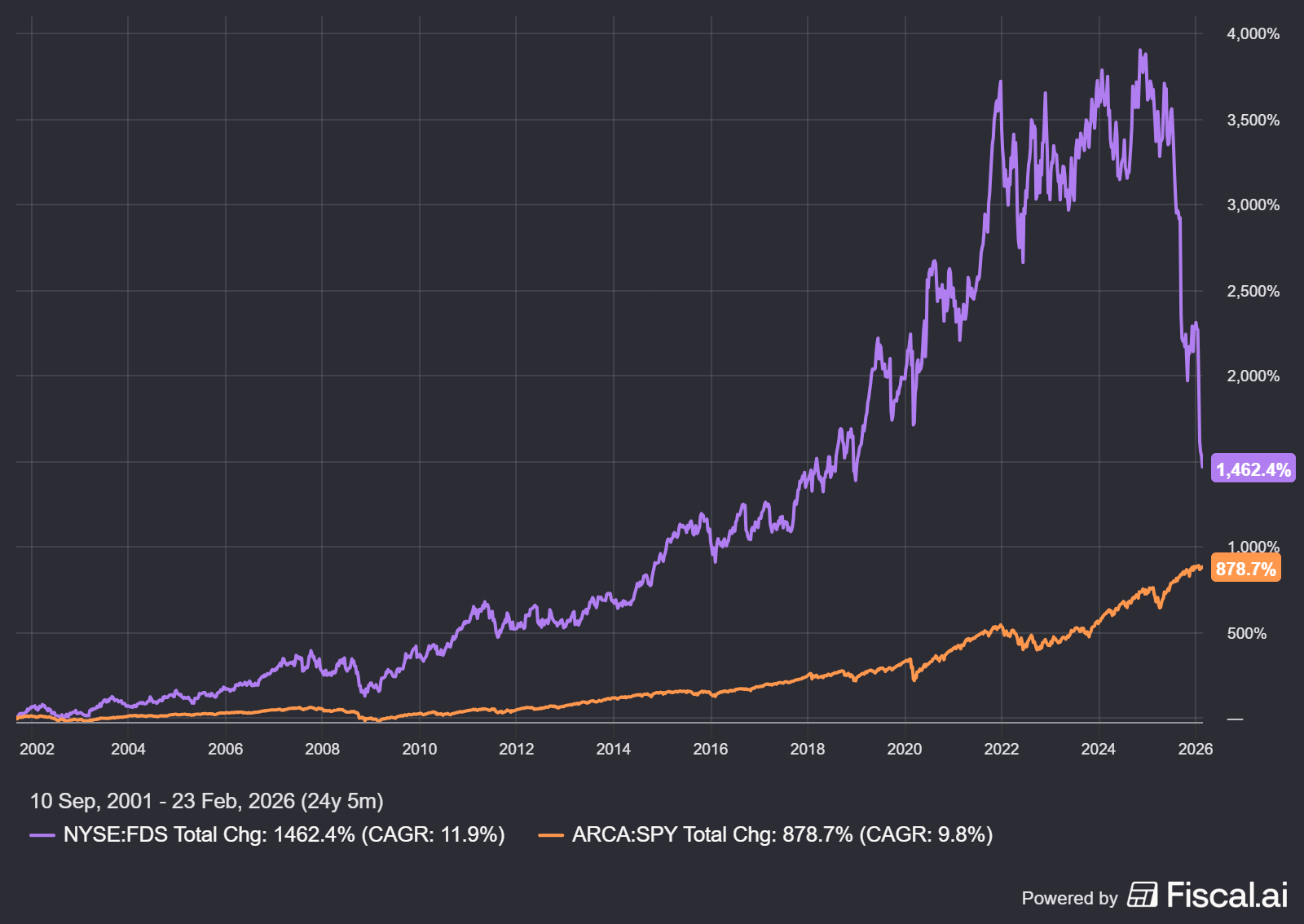

And yet, if we zoom out (as I prefer to do), since going public, FactSet has outperformed the S&P 500.

So yes — FDS has been heavily punished by the market.

Which leads to the next question:

Why Has FDS Been Hit So Hard?

I haven’t done a deep qualitative dive yet, but based on what I’ve read, these appear to be the main concerns the market is pricing in:

Broad fear around SaaS businesses in light of new AI tools.

Increasing competition: Bloomberg, or lower-cost data solutions for those of us who can’t afford premium platforms.

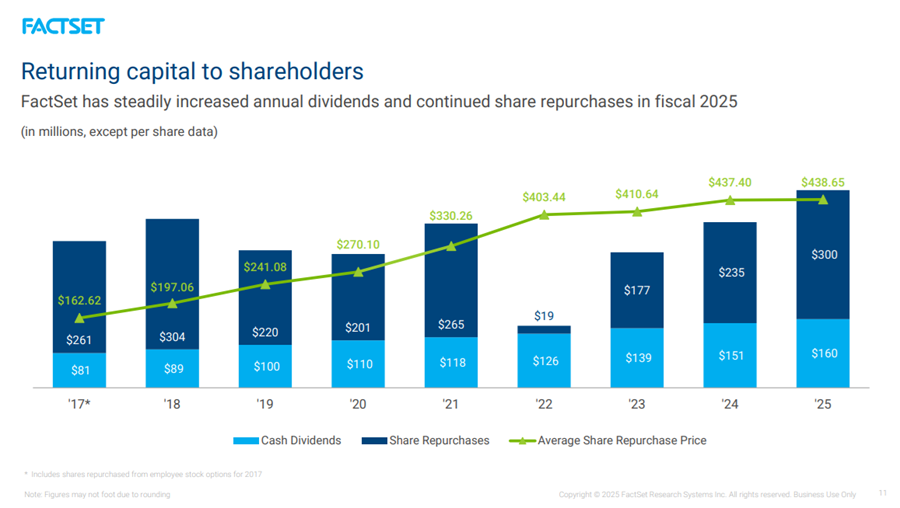

Somewhat “mediocre” capital allocation. FactSet generates a lot of cash but doesn’t seem to have many high-return reinvestment opportunities (at least in theory). So how does it reward shareholders? By paying and steadily increasing dividends. That’s the “mediocre” part.

On the positive side, the company has also been repurchasing shares using internally generated cash — without taking on debt. Yes, sometimes at prices that were arguably “expensive.” But more recently, buybacks have accelerated as the stock price has fallen.

And yes — shares outstanding have declined meaningfully over the past decade.

So… What Is FactSet Worth?

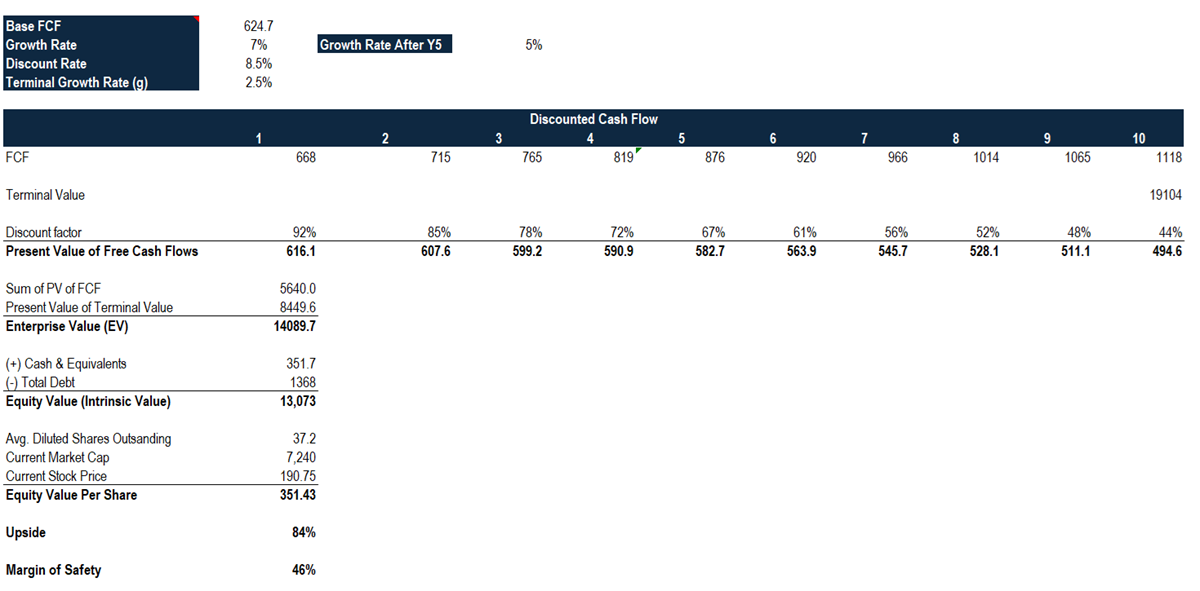

I ran a DCF valuation using my normalized economic numbers (not the reported accounting figures you’ll find on financial data platforms).

In short, at current levels, the market price implies a significant discount relative to my estimated intrinsic value. In my model, that translates into roughly 84% potential upside.

Important: I’m not assuming heroic growth, margin expansion, or multiple expansion. The model uses growth rates broadly in line with the company’s historical averages, followed by gradual deceleration. There’s no “magic catalyst” embedded.

This is simply a quantitative reading of the business under reasonable assumptions.

Conclusion

FactSet is not an operationally broken company. It’s a business with high returns on capital, strong margins, consistent cash generation, and a long history of value creation.

Yet today, the market is pricing it as if it faces meaningful structural deterioration.

The question isn’t whether FactSet is a good business.

The question is:

Is the market overestimating the long-term structural risk from AI and competition… or am I underestimating something important?

The enterprise value seems to be almost $9b and the FCF is like $600m per year?

How did you calculate the 10Y average EV/FCF multiple of 3x?

What am I missing?